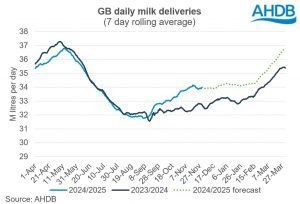

Last month, we reported on how farmers curbing production at the request of their buyers reduced April production. With the latest available data, the estimated amount cut from April production has been revised from 23 million litres to 19 million litres. For May, we estimate that production was 36 million litres lower than if a portion of farmers hadn’t curbed their production.

Post-peak, there continues to be a gap between where we would have been and where we are. This shows that it hasn’t been so easy to turn the tap back on again. However, there have been some differences between the reducer companies and non-reducers, which has closed the gap marginally. The average week-on-week decline (week ending 16 May to w/e 6 June) was -0.9% for reducers but -1.2% for non-reducers, our estimates suggest.