In the world of COVID-19, things tend to move quickly.

One week travel and social catch-ups are in place — and then the next, snap-lockdowns and border closures are the new norm. In light of all these changes, Australian’s love for dairy has remained consistent, as reported in Dairy Australia’s latest Situation and Outlook report.

Whilst domestic dairy demand overall has remained strong throughout this pandemic, some changes have emerged which are impacting the broader supply chain.

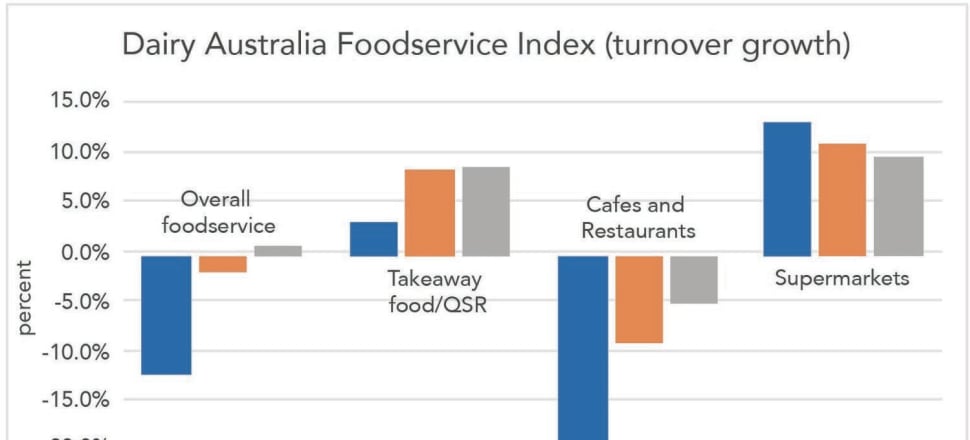

One of these key changes is where consumers like to spend their money. During the three months to March, Australians spent slightly more (0.8 per cent) in foodservice channels than the same period in 2019.

Café and restaurant demand has started to improve, however continues to track lower than before the pandemic. Takeaway and quick service restaurants remain the catalysts for the recovery in overall foodservice sales, as consumers across the country continue to prefer to eat their meals at home.

Generally, more dairy is used in these outlets — for example, shredded cheese on pizzas — and thus consumers’ move to these shops is supporting dairy product demand.

Alongside a shift in where consumers spend their money, there has been a notable pivot in what sort of products people buy. During the past year, consumers have grown increasingly mindful about their spending habits and are taking more care when choosing what products to buy. This has led to consumption changes and seen an increased focus on branded products over private label variants.

Everyday-style cheese sales grew 3.7 per cent in volume in the past year to 18 April, due to a rise in demand for branded packs, which was up nine per cent. In comparison, sales of private label everyday-style cheese only grew 0.3 per cent. A similar trend can be observed in the sales of most dairy products.

This development has been apparent across almost all income levels, with only above average and high affluence households increasing their purchases of private label products. These groups bought more private label fresh milk and Greek-style yoghurt in the past year, while people in lower income brackets turned to branded products.

This is a marked change to usual sales patterns, as low affluence households tend to be overrepresented as buyers of private label products. This signals a potential change in what consumers favour when making shopping decisions, leading to improved value creation opportunities for the industry.

Additionally, consumers continue to shop less often than before this pandemic and opt for more planned trips. As such, they are buying more and larger pack sizes each time they shop, at the expense of smaller pack sizes and more frequent store visits. Dairy Australia’s domestic sales data also shows that sales of three-litre milk bottles grew faster than smaller pack sizes, up 5.8 per cent in the six months to February compared to the year prior.

The dairy industry as a whole has so far managed to navigate its way through COVID-19 disruptions reasonably unscathed. With the pandemic being far from over, rapidly changing restrictions are likely to remain part of our ‘new normal’.

Encouragingly, consumer demand for dairy products appears reliable no matter the latest COVID-19 development. An increased focus on branded products by consumers also bodes well and is likely to support returns through the supply chain going forward.