Milk prices remain much lower than those enjoyed last year, the average Defra price sat at 37.0ppl for Oct 23. The expectations for the rest of the milk year are that now that with a continued lower milk price and still eye-wateringly expensive input costs, many farmers could be facing a winter crisis in cash flows. This will be further exacerbated by higher interest rates meaning an increased cost of borrowing. In addition to that many will be hit with a bumper tax bill following the last year of high milk cheques.

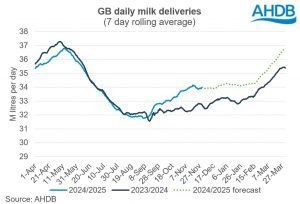

So far, these reductions have been driven by yield reductions, rather than herd size as cow numbers have remained stable. However, until prices begin to recover/or input costs reduce significantly (and probably unrealistically) there will be little incentive for farmers to push cows. We could yet see herd reductions in the Winter which could further exacerbate production levels. Overall, our expectation is for tightening supply through until the next milk year. This could start to ease if prices begin to pull back.

Latest wholesale prices would indicate that milk prices could begin to move in a more positive direction in the first quarter of the new year, but the extent to which they might recover remains uncertain and much will depend on the recovery of global demand.