On the international stage, the competitiveness of Australian dairy products somewhat improved over the 2023-24 season — tighter global supply supported international export pricing and shipping challenges along key routes diverted additional demand towards Oceania product.

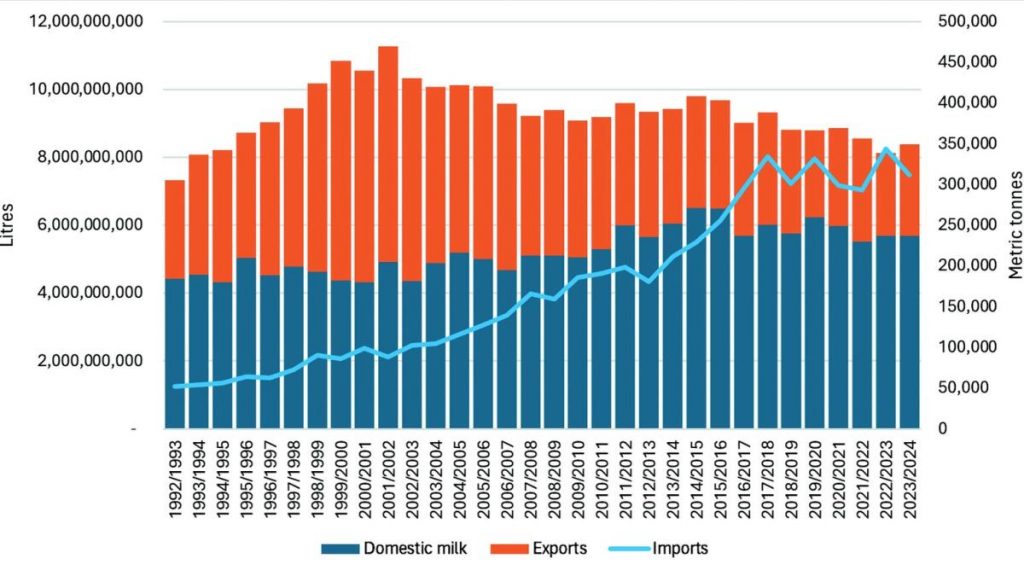

Nevertheless, Australian dairy exports only increased one per cent last season, totalling almost 705,000 tonnes.

Purchasing activity from importers globally has become more price sensitive as costs bite across the supply chain, and China’s own economic woes (and strong local production) continue to weigh on the dairy export market.

As such, Chinese buyers purchased 30 per cent less Australian dairy over the season, with other key markets soaking up the balance.

Product shipped to Japan increased 22 per cent, supporting total cheese exports, and buyers across the South- East Asia region imported 23 per cent more Australian dairy than in the 2022-23 season.

At the same time, Australian dairy remained under pressure from overseas product domestically.

Almost 312,000 tonnes of dairy was imported into Australia over the 2023-24 season; while this was nine per cent lower than the previous season, it was still higher than the two seasons prior.

There are a variety of reasons overseas dairy products are imported into Australia, with economic factors being a key driver in recent years.

Considering Australia’s modest milk production recovery, improved product competitiveness and shipping challenges (impacting the flow of product into Australia, not just out), less dairy was sourced from New Zealand (-7 per cent), Europe (-7 per cent) and the United States (-24 per cent) over the 2023-24 season.

The 2024-25 season is now under way, bringing with it some new developments (lower farm gate milk prices) and some old aspects (weather and economic challenges).

Considering the impacts these may carry for milk flows this season, Dairy Australia is forecasting total production to drop slightly, maintaining a national milk pool around 8.3 billion litres.

Economic challenges will likely remain a feature of dairy markets in the months to come — with limited recovery in export markets foreseen in the near term, regaining domestic market share will likely be a focus for many manufacturers.

Eliza Redfern is Dairy Australia’s Analysis and Insights manager.

You can now read the most important #news on #eDairyNews #Whatsapp channels!!!

🇺🇸 eDairy News INGLÊS: https://whatsapp.com/channel/0029VaKsjzGDTkJyIN6hcP1K